Schedule D, Part 2, Section 2 – NAIC Validations for Mutual Funds (9499999), Unit Investment Trusts (9599999) and Closed-End Funds (9699999):

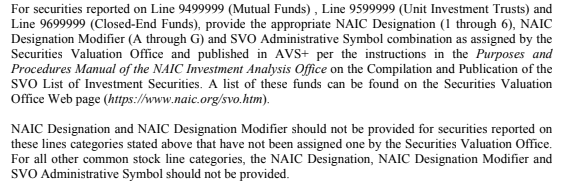

The Annual Statement Instructions for Schedule D, Part 2, Section 2, Column 18 are as follows:

For those securities that fall into the second paragraph, where an NAIC designation has not been assigned by the SVO, Column 18 should be left blank. Leaving column 18 blank, however, will trigger a validation for NAIC rules PTASU900100, PTASU900101 and PTASU900102 (for Life customers, the same rules apply but the “P” would be replaced by an “L”). This validation was brought to the attention of the NAIC at the end of 2020 and they responded with the following comment “if a company fails because they don’t have an NAIC designation category or administrative symbol, they should include an explanation. This is why the crosscheck in the instructions to tie these columns to the new footnote was removed on Sch D, Part 2, Section 2“.

Example Explanation: An example of an appropriate explanation may read: “An NAIC designation has not been assigned by the SVO” or something to that effect.

This situation is obviously not ideal, but the above practice of providing an explanation for this validation will need to be followed for the 2020 Annual.

The NAIC has recognized that this is not ideal and the Blanks Working Group (BWG) has an exposure draft, currently out for public comment, to remedy this situation for possible implementation effective 1st Quarter 2022. Agenda item #2020-35BWG is, among other things, recommending the following: Split the line categories for Mutual Funds, Unit Investment Trusts, and Closed-End Funds into lines indicating if the fund has been assigned a designation by the SVO or not. This split should alleviate the validation errors.

As always, Gain Compliance integrates the latest changes into the NAIC guidelines to streamline the reporting process. If there are any further questions or comments, please do not hesitate to reach out.

Make sure to check out our other blog posts, and follow Gain Compliance on LinkedIn, Facebook and Twitter.