Photo and data credit to CB Insights

Unicorns are very rare.I’m not talking about the conventional, fairy-tale animal, but rather the Silicon Valley definition:

A unicorn is a startup valued at over $1 billion. The term was coined in 2013 by venture capitalist Aileen Lee, choosing the mythical animal to represent the statistical rarity of such successful ventures. (Citation)

If you’re an investor, two important questions arise:

Just how uncommon is this outrageously good outcome?

And, even more importantly, what are the likelihoods of other outcomes?

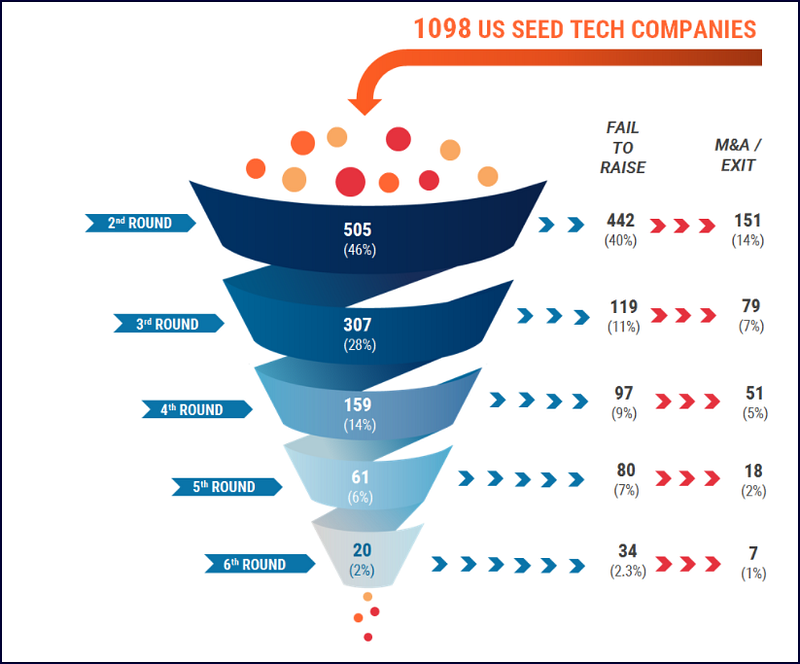

Through tracking the outcome of 1,098 startups who raised financing between 2008 and 2010, CB Insights pegs the odds of a unicorn outcome at less than 1%.

Source: CB Insights

A few key takeaways from dissecting these results:

- This data set ignores the class of startups — likely a majority overall — who fail to raise even a first round of financing.

- Of the companies who reached this milestone, only 46% succeeded in raising a second round.

- The outcomes for those did not raise a second round? A portion of this group (14% of total sample) realized some sort of exit by being acquired. While good data is hard to find on the outcomes of the rest (40% of companies in the overall group), it’s safe to assume that the overwhelming majority ended up as roadkill.

- Slightly more than 70% of startups who raised an initial round failed to either raise additional financing at some later date or achieve an identifiable exit.

Overall, the odds are tough. Interestingly, early success is not a guarantee — or even much of an indicator— of a profitable outcome.

Let’s say, following the above graphic, you invested in one of the companies who successfully raised a third of financing. This company has defied the odds, as roughly two out of every three of their tracked peers had failed to reach this milestone. If a company has made it this far, the odds are in its favor, correct?

Not so much.

Of the 307 companies who achieved this stage, two-thirds — 211 — will at some point fail to either raise a subsequent round or reach a liquidity event through acquisition or public listing.

And, even for the 96 who exit through an IPO or acquisition, this result is still no guarantee of financial success for stakeholders; this is entirely dependent on final valuation.

Focusing on this last point for a moment: it is not sound to assume that an acquisition or public stock listing equates to a profitable outcome. In this sense, this article actually paints too rosy a picture for founders, investors, and employees: even companies who manage to progress through the funnel do not always represent profitable outcomes.

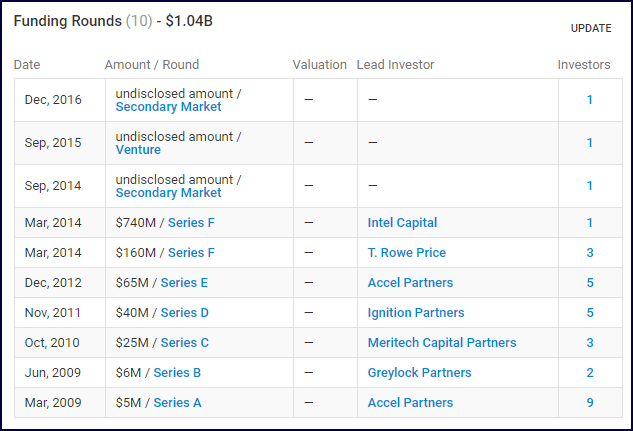

By way of example, take Cloudera (NYSE: CLDR) which recently completed an IPO after seven rounds of funding. Its current market cap is a little south of $3 billion. A happy ending for all involved, right?

Here’s what its funding history looks like:

Source: Crunchbase

Due to a heady valuation at the time of investment, the value of Intel Capital’s stake of $740 million (purchased at $30/share in March, 2014) was halved by the time of the IPO’s pricing (at $15/share) three years later. Similarly, any employee who was issued options at the time of the Series F round (at the fair market value at that time) found their grants to be deeply underwater at the celebration.

So, the numbers are pretty grisly in the market as a whole. But, this doesn’t mean that this will be the fate of any one startup (including, most importantly, yours, right?).

While hope springs eternal, and entrepreneurs famously have out-sized confidence in their personal abilities to succeed, the numbers are hard to ignore.

This begs the question:

Are there any ways for a startup improve its odds?

The answer is simple: yes, just take a different approach from the cohort tracked to compile these statistics. By nature of the data available, the 1,098 companies of the CB Insights data set disproportionately followed a traditional venture capital financing model. In doing so, these startups brought a great deal of unnecessary risk upon themselves.

Eric Paley, in his 2016 Tech Crunch article Venture capital is a hell of a drug, described a chief pitfall of this funding track in a single sentence:

Venture capital increases risks for founders.

Eric’s piece is a great read on a few levels, as he steps through the often-misaligned goals between startups and VC investors which lead to this conclusion.

And, just as important as the logic behind the need for venture capital to push portfolio companies to take on greater risk, are the benefits of doing so. It would be logical to think there is a necessary tradeoff, that embracing additional risk would increase the chances for a out-sized, unicorn-type outcome.

You can’t become a unicorn without taking on heightened risk, right?

Not so. Citing over a dozen examples, the article’s final punchline dispels this myth:

One argument I’ve heard from many VCs is that a founder won’t build a billion-dollar startup unless they go all-in from the start. This is nonsense — to become a billion-dollar business, a founder first needs to build a $10 million business. Founders shouldn’t jump to the end game before they’re ready. You focus on the first step and still become a huge player in the end.

As you might gather, this is a sentiment and path we wholeheartedly embrace at Gain Compliance — an appropriately careful and deliberate approach to building a company. Startups are tough enough without embracing unnecessary risk.

Make sure to check out our other the blog posts, and follow Gain Compliance on LinkedIn, Facebook and Twitter.